Support

Publications

These white papers have been created to help you keep on top of the latest industry developments. Take a look at some of our past publications.

White papers

In an industry that never stands still, we want you to keep on top of the latest developments and changes to current legislation and the market. We’ve created a series of white papers that set out the issues and key themes to be aware of, and the action you might need to consider.

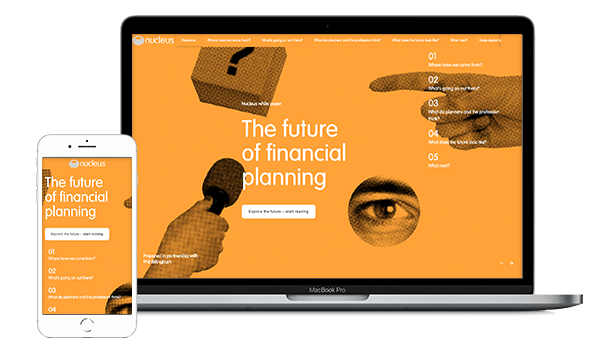

The future of financial planning white paper

To encourage debate around what may lie ahead for financial planning, we’ve compiled this interactive white paper with Phil Billingham of Perceptive Planning.

Behavioural white paper

This white paper, written in partnership with Neil Bage and Dr. Ariel Cecchi of behavioural insights firm Be-IQ, takes the principles of behavioural science and shows how they can be applied to the financial planning process.

Hubspot modal form settings

Change the portalId and formId numbers in the code below

Portal id: 316077

Form id: 5f9e1b8a-1481-4adc-a3ae-a6478620069c

Modal title: Download the behavioural white paper

Button text: Download the behavioural white paper

SM&CR – a guide for financial advisers

SM&CR came into force for all regulated firms in December 2019. The regime aims to provide greater protection for customers and strengthen market integrity in financial services. It looks to do this through greater individual accountability at every level of financial services firms, and in particular for those in senior management positions. Nucleus wrote this white paper, together with Phil Young of Zero Support.

Hubspot modal form settings

Change the portalId and formId numbers in the code below

Portal id: 316077

Form id: 99f50abd-140d-4ff2-ba09-c34b1befe09b

Modal title: Download the SM&CR white paper

Button text: Download the SM&CR white paper

Suitability - a guide for financial advisers

Suitability is the framework to deliver great client outcomes: it's the cornerstone of developing a consistent approach to advice, and extra reassurance to your clients that the recommendations you're making are suitable. Nucleus has compiled this white paper together with ex-regulator Rory Percival.

Hubspot modal form settings

Change the portalId and formId numbers in the code below

Portal id: 316077

Form id: 5483a7dc-f812-444d-ba87-b5ffbe3a1dfd

Modal title: Download the Suitability white paper

Button text: Download the suitability white paper

GDPR – a guide for financial advisers

The aim of GDPR is to make sure people have control of their data. You need to understand how this impacts your business, your clients, what data you hold and what you use it for.

Hubspot modal form settings

Change the portalId and formId numbers in the code below

Portal id: 316077

Form id: 8a698780-9ae5-4c12-93ee-d189dd4625b6

Modal title: Download the GDPR white paper

Button text: Download the GDPR white paper

MiFID II a guide for financial advisers

MiFID II aims to dramatically reduce the risk of market abuse, strengthen investor protection and increase the efficiency of financial markets. It covers a broad range of issues - we've focused on those that are most likely to affect you as advisers.

Hubspot modal form settings

Change the portalId and formId numbers in the code below

Portal id: 316077

Form id: d974b570-5e8f-49dc-aa6c-5072ca939ab7

Modal title: Download the MiFID II white paper

Button text: Download the MiFID II white paper

Planning your exit: A guide to creating a succession plan and exit strategy

Our white paper provides you with information on getting started on developing a succession plan for either internal succession or external sale, what the options and challenges really are, and how to create and execute an effective exit.

Hubspot modal form settings

Change the portalId and formId numbers in the code below

Portal id: 316077

Form id: 249aa3b5-1bd8-476d-8078-892808a28bbd

Modal title: Download the succession white paper

Button text: Download the succession white paper

Getting in touch with us couldn't be easier

Are you interested in becoming a Nucleus user? Then simply click on the button below to contact one of our regional business development directors who'll be delighted to help. If you're an existing user, hit the button below to download your regional contact sheet.